At the start of the year, industry analysts predicted that production would pivot from predominantly refinances to purchase around the middle of the year. Recent MBA Origination Insight Reports have begun to show the scale starting to tip towards purchase loans. Now, the MBA’s “Mortgage Finance Forecast,” released on August 20 and covering the next 18 months, is predicting that the refinance share of the market will drop to 28% in Q4 this year, and purchase originations will dominate between 70% to 75% of business for 2022.

Are you and your team ready to build your business around the purchase market for at least the next 18 months?

Even if your business has been doing purchase loans regularly, having a high mix of refinance loans has given the team some breathing space in between purchase loans. With a predominantly purchase business, they’ll be dealing with many more emotionally fraught consumers at various stages of readiness and with time constraints to close their loan.

Fortunately, there are fintech solutions that can help your team not just cope but thrive in this market. Many small to medium-sized lenders won’t be able to pivot unless they adopt technology to stay competitive.

If you haven’t implemented a digital mortgage application process over the past 18 months while the team was working from home, you can’t afford to put that decision off any longer. First-time homebuyers in their 20’s and 30’s expect the convenience of a digital mortgage application. They will go to your competitors or one of the big mortgage advertisers if you can’t provide this service.

When you obtain potential homebuyers at the top of the sales funnel, they come to you at various stages of mortgage readiness. Moving up homeowners are more likely to be mortgage eligible when you connect, but the pandemic could’ve affected their savings, credit, and employment history. Most first-time homebuyers will likely need guidance through the entire mortgage process and have at least one financial hurdle to overcome before they can start their home search.

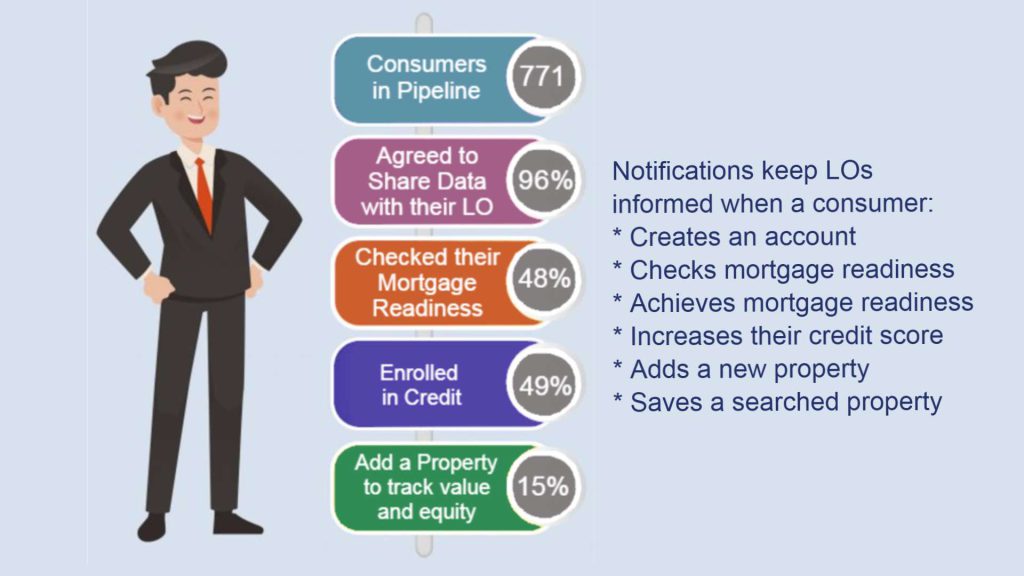

To help originators nurture homebuyers and close more purchase loans, FinLocker has integrated all of the tools a first-time homebuyer needs to get mortgage-ready. The originator simply invites every homebuyer who isn’t ready to download their branded FinLocker. While the potential homebuyer interacts with the tools to improve their mortgage eligibility, other built-in widgets can be your digital assistant, educating them on the mortgage process, loan products and providing a monthly mortgage payment and home budget that fits their income. They can even start their home search from your branded FinLocker app, so there’s no need to use any of the other lead-grabbling finance / real estate apps.

What’s more, the whole FinLocker platform ingrates with your LOS to streamline the digital mortgage application for tech-savvy first-time homebuyers, saving your entire operations team time and reducing risk. And, the platform is affordably priced, enabling small to medium-sized mortgage lenders to compete with the top national lenders’ technology.

Watch the self-service FinLocker demo to learn how FinLocker can help your business pivot to compete in the purchase market, then schedule a demo or consultation to have your questions answered.